The Fed’s Daring Gamble: A Quarter Point Cut That Echoes Across the World

The Federal Reserve’s decision to lower interest rates, the first cut since 2024, is far more than a technical adjustment; it is a powerful…

The Federal Reserve’s decision to lower interest rates, the first cut since 2024, is far more than a technical adjustment; it is a powerful signal that ripples through every layer of the American and global economy, altering the calculus for everyone from Wall Street titans to first-time homebuyers.

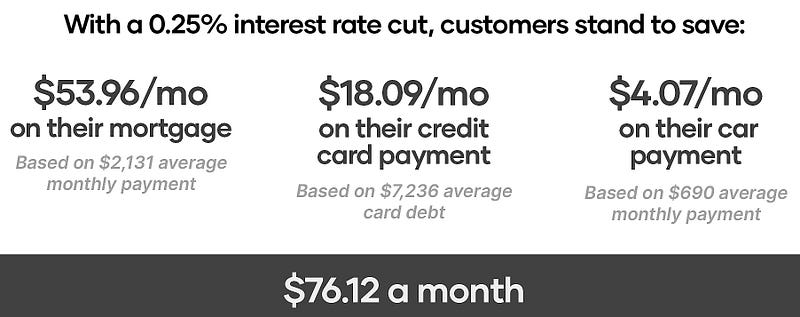

For the macro-economy, this move is a preemptive strike against slowing growth. By making borrowing cheaper, the Fed aims to stimulate economic activity. Businesses, large and small, are incentivized to take out loans for expansion, new equipment, and hiring. This injection of capital seeks to boost corporate investment and, ultimately, job creation. For the government, the cost of servicing the immense national debt becomes slightly less burdensome, freeing up fiscal resources. Consumers, the true engine of the U.S. economy, are confronted with a new financial landscape. Loans for cars, credit cards, and most significantly, mortgages, become more affordable, encouraging spending and investment in big-ticket items. This attempt to reinvigorate demand is the Fed’s primary tool to ward off the specter of a recession and extend the economic cycle.

On a micro level, the impact is intensely personal. For any individual with variable-rate debt, from a small business line of credit to a homeowner with an adjustable-rate mortgage, their monthly payments will decrease, putting more cash in their pocket. This immediate boost to disposable income can increase consumer confidence and retail spending. Conversely, savers and retirees who rely on interest income from savings accounts, CDs, and bonds will feel the pinch, as their returns diminish practically overnight. This creates a push factor, encouraging them to seek higher returns in the stock market, which itself is reacting violently to the news. Equity markets typically rally on lower rates, as future corporate earnings are discounted at a lower rate, making stocks more attractive relative to fixed-income alternatives. The housing market is poised for a fresh surge, as lower mortgage rates improve affordability and can push property values higher, widening the wealth gap between homeowners and renters.

Globally, the Fed’s decision sends a tidal wave across international markets. A U.S. rate cut often weakens the dollar, as lower yields make dollar-denominated assets less attractive to foreign investors. A weaker dollar provides an immediate boost to American exporters, making their goods cheaper abroad, but it simultaneously makes imports more expensive, potentially fueling domestic inflation. For emerging markets, the move can be a double-edged sword. It eases pressure on their own central banks to maintain high rates to defend their currencies, allowing them to also stimulate their economies. It can also trigger a flood of capital seeking higher returns, boosting their asset prices. However, it also increases the risk of asset bubbles and financial instability. For other developed nations, like those in the Eurozone, it creates policy divergence, forcing them to navigate their own economic challenges amidst a shifting global monetary tide.

Ultimately, this quarter-point cut is a statement of both confidence and concern — confidence that the U.S. economy is strong enough to avoid overheating, but concern that without a nudge, its momentum might falter. It is a gamble that cheaper money will fuel productive growth rather than merely inflate new asset bubbles, a decision whose true impact will unfold in the months to come, shaping the financial fate of millions.