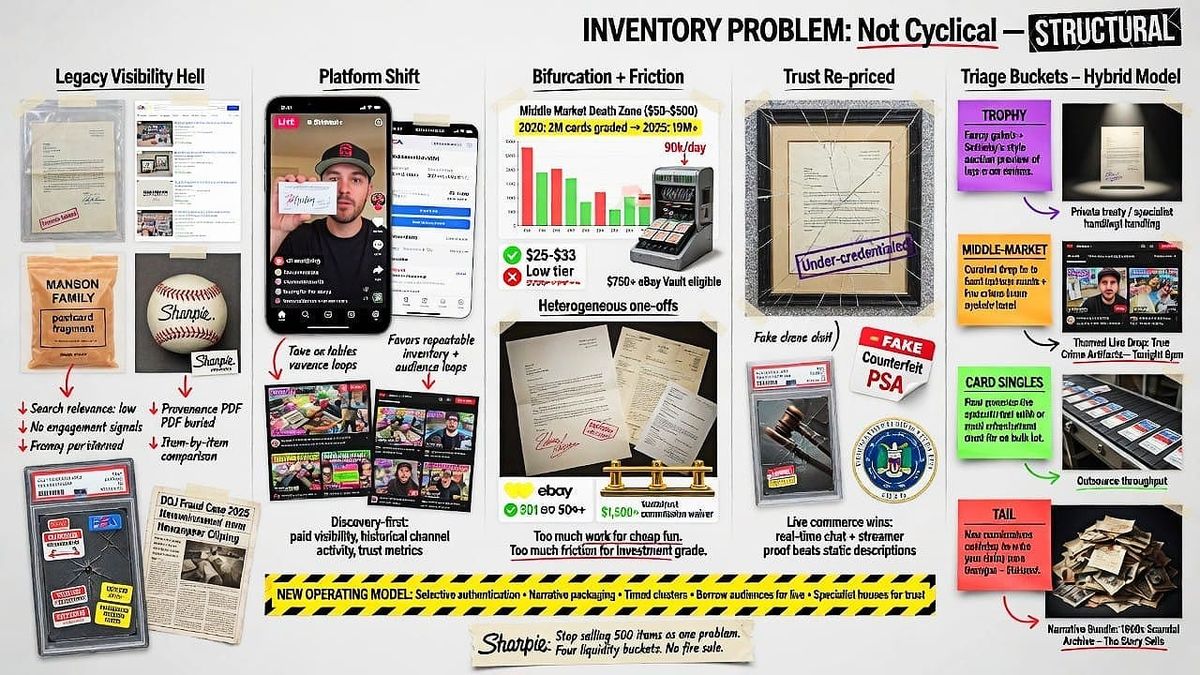

Liquidating a Five-Hundred-Item Collectibles Inventory in a Discovery-Driven Market

The “new way” is a hybrid operating model: authenticate selectively, package narrative aggressively, sell in timed clusters, use specialist houses where institutional trust matters, and borrow existing audiences for live commerce rather than trying to build one from scratch.

Executive Summary

The inventory problem is not just cyclical. It is structural. Over the last five years, collectibles selling has moved from a market organized primarily around explicit search and item-by-item comparison to one increasingly organized around recommendation systems, live feeds, creator-led selling, and paid visibility. On legacy marketplaces, visibility still depends on search relevance, listing completeness, seller performance, and item popularity; on discovery-first platforms, it depends even more heavily on predicted engagement, watch time, historical channel activity, conversion probability, and trust metrics. That shift favors continuous sellers with repeatable inventory, strong audience loops, and advertising or livestream infrastructure. It punishes the exact kind of inventory described here: heterogeneous, one-off, middle-market, and provenance-sensitive items that do not produce stable engagement signals at scale.

At the same time, the market has bifurcated. Platforms have built premium trust rails and financial infrastructure around higher-value material: eBay trading-card authentication begins at $250, the eBay vault was launched for qualifying graded cards bought at $750+, and Whatnot currently waives base commission on the portion of eligible orders above $1,500 in key collectibles categories. Meanwhile, grading and selling costs have become industrial-scale inputs. PSA says it graded 2 million cards in 2020 and more than 19 million in 2025, with current capacity around 90,000 cards per day, while its low-end card-grading tiers now cost roughly $25 to $33 per card. That makes the middle market economically fragile: a $50–$500 item often bears too much friction to be “investment grade” and too much work to be “fun cheap inventory.”

Trust has also been re-priced. PSA explicitly says demand has been accompanied by a rise in sophisticated fraud and counterfeiting; counterfeit slabs remain a known issue; DOJ cases in 2025 show that forged memorabilia remains an active criminal market; and eBay’s own card-authentication rules make clear that even when eligible cards receive Authenticity Guarantee, in-person autographs and aftermarket relics are not what the service is actually verifying. In that setting, static listings for autographed letters, true-crime pieces, and historical artifacts are not merely old-fashioned. To many buyers, they are under-credentialed. Live commerce has gained ground because real-time presentation, chat, social proof, and streamer interaction create trust transfer that static catalog descriptions often cannot match.

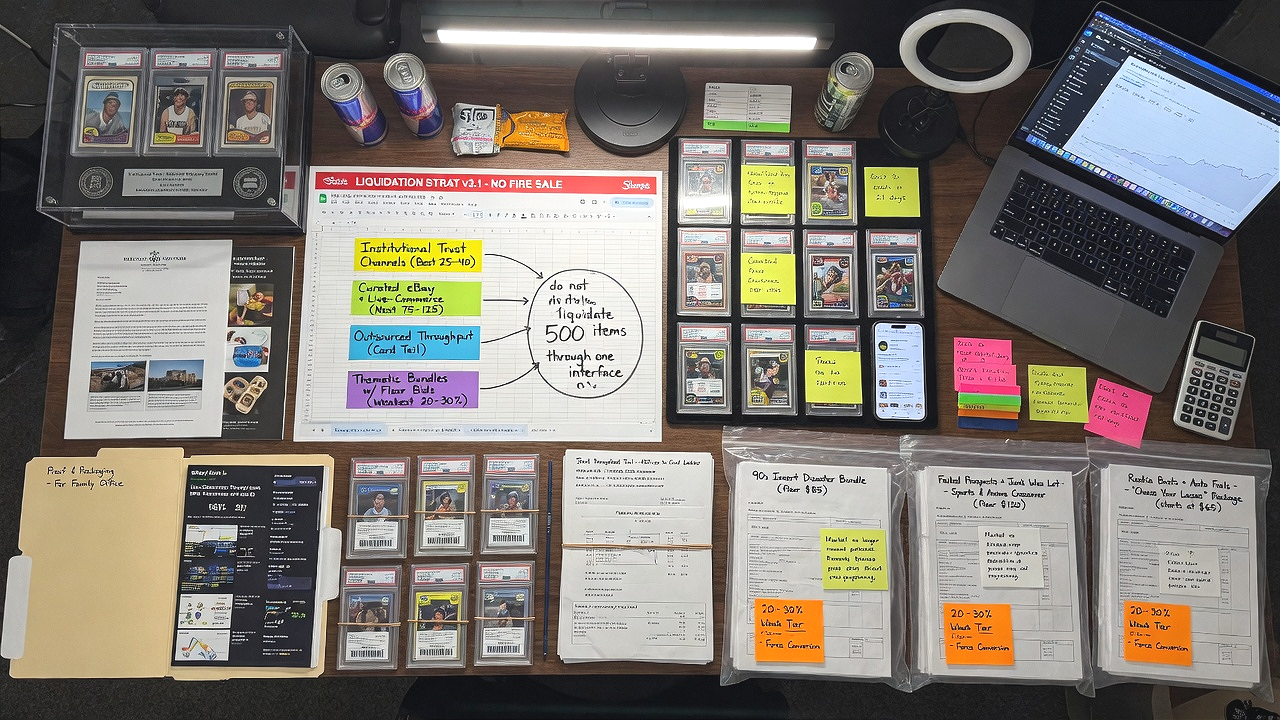

The right response is not a fire sale. It is inventory triage. The seller should stop treating the 500 items as one marketplace problem and start treating them as four distinct liquidity buckets: trophy items that deserve specialist auction or private-treaty handling; strong middle-market items that can be eventized into curated drops; standardized card singles that can be outsourced for throughput; and tail inventory that must be bundled thematically so that the story, not the single item, becomes the unit of sale. The “new way” is a hybrid operating model: authenticate selectively, package narrative aggressively, sell in timed clusters, use specialist houses where institutional trust matters, and borrow existing audiences for live commerce rather than trying to build one from scratch. That is how a seller regains liquidity without accepting blanket wholesale pricing.

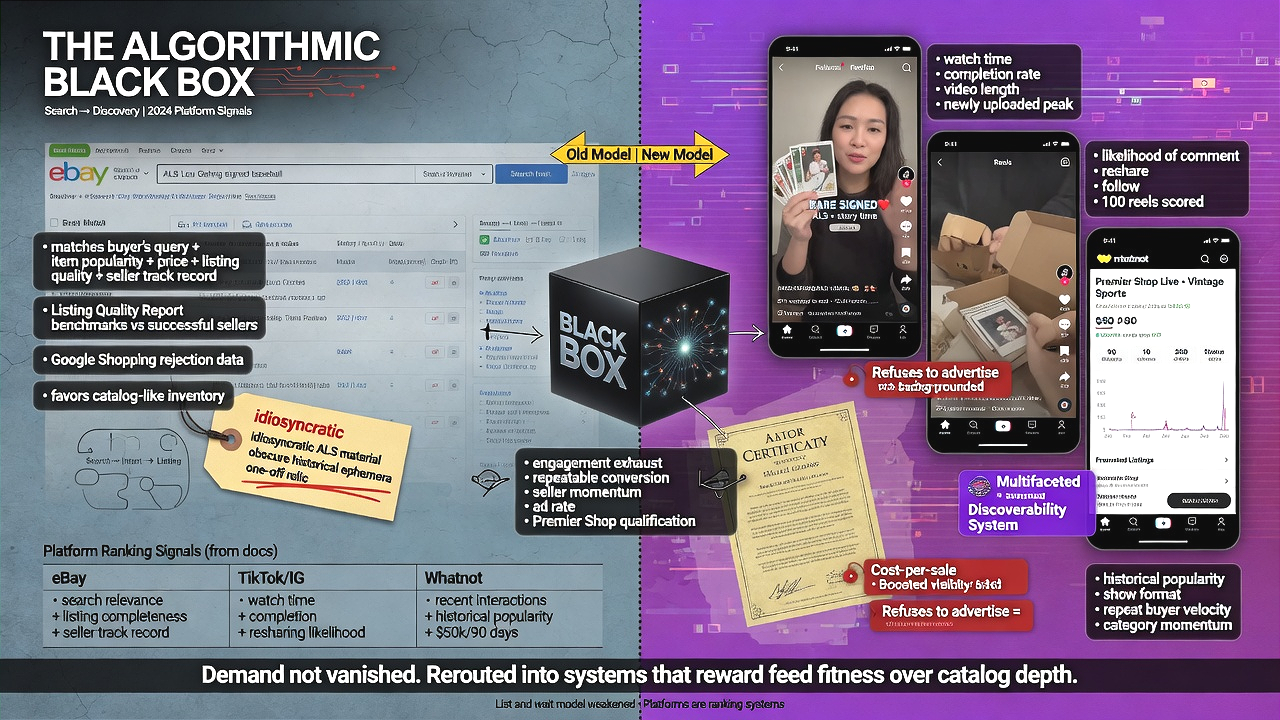

The Algorithmic Black Box

The old search-based model is still visible on eBay. The company says Best Match considers how closely a listing matches the buyer’s query, item popularity, price, listing quality, listing completeness, service terms such as returns and handling time, and the seller’s track record. eBay also tells sellers that its Listing Quality Report benchmarks them against what the most successful sellers are doing and recommends actions to improve search impressions, views, and sales; the report even incorporates Google Shopping rejection data. In plain English, the system is not only asking, “Is this item relevant?” It is also asking, “Does this listing look structured, standardized, and commercially proven?” That favors catalog-like inventory and disciplined listing operations. It does not naturally favor idiosyncratic ALS material, obscure historical ephemera, or a one-off relic that needs context to make sense.

Discovery-based commerce works differently. TikTok says its For You feed ranks videos based on user interactions, video information such as captions, sounds, and hashtags, and lower-weight device/account settings; it also states that strong interest signals like completion of longer videos carry more weight than weak contextual signals. TikTok further tells creators that watch time matters materially for recommendation and that newly uploaded videos typically see a peak soon after publication. Meta’s Instagram Reels ranking documentation says the system gathers candidate reels, uses signals such as reel length and similarity, predicts relevance, and ranks approximately 100 reels by score; its predictions explicitly include the likelihood of viewers watching past thresholds, commenting, resharing, or following the creator. This means that discovery commerce rewards content that behaves like media. The item has to win attention before it can win a transaction.

Whatnot makes the mechanism even more explicit because it is both a marketplace and an entertainment feed. The company says it uses a “multifaceted discoverability system” and that signals include users’ explicit and implied interests, seller quality metrics, listing quality, shipping speed, refund rate, cancellation rate, show format, and category. In the For You feed, it predicts views, bids, and orders; among the most important signals are seller category, average order value, recent interactions with the seller, and recent interactions with that seller’s top category. In the Followed Hosts and category feeds, Whatnot says shows are ordered by “historical popularity,” meaning how much activity the channel has generated in the recent past. Its Premier Shop program intensifies the same pattern: to qualify, a U.S. seller needs at least 90 days on platform, 10 shows, 250 orders, and $50,000 in sales over the prior 90 days, after which their products and shows are eligible for more prominent placement in search and recommendations.

That is the black box in practical terms. A middle-market collector with one-of-a-kind inventory is not merely competing on item quality. He is competing against systems that prefer repeated proof of engagement, repeatable conversion behavior, and seller-level momentum. A rare signed ALS may be “better” than a stream of commodity singles, but it creates none of the behavioral exhaust that discovery systems love: no category velocity, no repeat buyers, no channel history, no consistent average-order-value signal, and no scalable ad economics. The unique item has to clear a higher storytelling bar just to be seen.

A second structural issue is paid visibility. eBay’s Promoted Listings program is explicit: it is an advertising service; sellers can boost the likelihood that listings appear “throughout the eBay buyer flows”; campaign funding can be cost-per-sale or cost-per-click; and placement/ranking are influenced by ad rate, quality, relevancy, and competing listings. That does not make organic discovery impossible. But it does mean visibility is increasingly auctioned or rented. Unique sellers who refuse to advertise, or who cannot justify advertising on low-velocity one-offs, are gradually pushed into the background while higher-margin, replenishable, or professionally merchandised inventory occupies more premium real estate.

The result is not that search is dead. It is that search is no longer sovereign. eBay still tells sellers that auction format is useful when an item is unique or hard to find, which remains true. But the commercial center of gravity has shifted from “list the item and let search route intent to it” toward “manufacture attention, prove trust, and convert in-feed.” That is why a seller who built a business in the search era experiences today’s market as if demand has vanished. In many cases demand has not vanished; it has been rerouted into systems that privilege feed fitness over catalog depth.

| Platform or rail | How discovery works | Load-bearing ranking inputs | What this means for one-off middle-market collectibles |

|---|---|---|---|

| eBay Best Match | Search-led | Query relevance, popularity, price, listing quality/completeness, service terms, seller record | Good for known-demand items with solid comps; weaker for obscure material with thin keyword demand |

| eBay Promoted Listings | Search plus paid placements | Ad rate or bid, relevance, quality, competition | Visibility can be purchased, which advantages scalable inventory |

| TikTok For You | Recommendation-led feed | Watch time, completion, interactions, captions/sounds/hashtags | The item must function as compelling content, not just inventory |

| Instagram Reels | AI-ranked feed | Similarity, watch behavior, comments, shares, follows, recent activity | Visual storytelling and social response drive reach |

| Whatnot For You / category feeds | Live-commerce feed | Predicted views, bids, orders; seller quality; average order value; historical popularity | Strongest for sellers with cadence, repeat audience, and channel momentum |

The mechanics in this table come directly from platform documentation and are the core reason the “list and wait” model has weakened. The platforms are not neutral shelves. They are ranking systems optimizing for relevance, engagement, trust, and monetization.

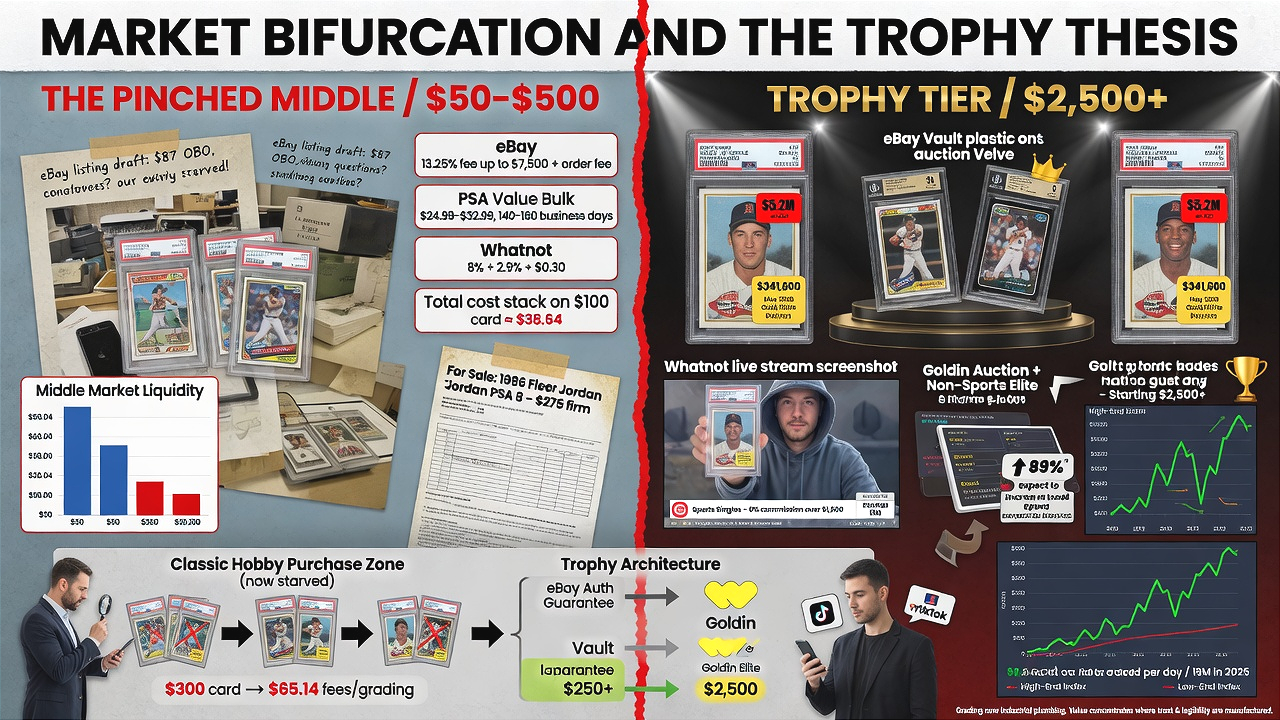

Market Bifurcation and the Trophy Thesis

The market is splitting because platforms, buyers, and infrastructure providers now treat high-end collectibles as a different asset class. The clearest evidence is the threshold architecture built into the market itself. eBay’s card Authenticity Guarantee starts at $250; eBay’s vault launched for qualifying graded cards purchased at $750 or more; Whatnot’s seller-fee schedule for Sports Singles and related categories now charges 8 percent commission up to $1,500 and 0 percent on the portion above that threshold, at least under its current high-value-orders promotion; and Goldin’s own marketplace architecture separates a low-entry weekly auction from elite auctions, with “Non-Sports Elite and Vintage Elite” positioned at $2,500 and up. Those are not arbitrary product settings. They are institutional signals that capital, trust, and concierge treatment are concentrated around expensive inventory.

The grading economy reinforces the same split. PSA says card grading demand has surged from 2 million cards in 2020 to more than 19 million in 2025; it currently grades about 90,000 cards per day globally; and its February 2026 pricing update moved low-end card services to roughly $24.99 for Value Bulk and $32.99 for Value. In May 2026 PSA said the hobby’s extraordinary growth had outpaced expansion, that collectors were on pace for another submission record, and that Value Bulk had moved to a 140–160 business-day completion range. This matters because grading used to be a selective enhancement. It is now part of the industrial plumbing of the hobby. When millions of cards are slabbed, grading does not merely certify rarity; it often manufactures a visible sorting mechanism that channels buyer attention toward the top condition census and away from everything else.

That is the heart of the trophy thesis. In a thick grading-and-ranking environment, value concentrates in the top of the distribution because the top is easy to explain and easy to trust. The finest copy, the elite slab, the famous name, the highest-grade rookie, the authenticated-and-vaultable item: these products are institutionally legible. By contrast, the lower 99 percent of the market is not literally worthless, but much of it becomes operationally illiquid. The seller still has to photograph it, write it, ship it, answer messages about it, and absorb fees on it. The buyer still has to overcome authenticity risk, condition ambiguity, and uncertainty about future resale. That combination compresses the market into a narrow set of items that are either obvious trophies or obvious impulse buys. The old $50–$500 “serious hobby purchase” gets pinched in the middle.

The economics are unforgiving. On eBay, a trading-card sale in the relevant categories is currently 13.25 percent of the sale amount up to $7,500, plus a per-order fee; on Whatnot, Sports Singles are 8 percent commission plus 2.9 percent processing and $0.30; PSA’s cheapest card grading tiers now sit around $25 to $33 before shipping, insurance, and time. Even before labor and postage materials, a $100 card sold on eBay and pre-graded through PSA Value Bulk can already carry roughly $38.64 in grading-plus-platform cost. At $300, the same simplified platform-and-grading cost is roughly $65.14. The ratio improves as price rises. That is exactly why the middle market feels starved: the cost stack is not linear in emotional pain, and the trust enhancement from grading or authentication only becomes obviously worth it once the gross price is high enough.

Card Ladder’s public pages illustrate how sharply the premium concentrates. Its index page currently shows the Card Ladder High-End index outperforming the Low-End index on its most visible recent-change slices, and its individual card pages show extreme separation between top-grade trophies and lesser copies. A 1952 Topps Mickey Mantle PSA 9 page shows a last sold price of $5.2 million in January 2021, while a PSA 1 page shows a listed best-offer price of $33,500; a 1986 Fleer Michael Jordan PSA 10 page shows a last sold price of $341,600 in May 2026. These are not the whole market, and iconic cards are obviously the most dramatic examples. But they are clean evidence of how grade, scarcity, and recognizability create an elite collector tier that behaves differently from the rank and file.

Buyer composition has moved in the same direction. eBay’s 2025 Recommerce Report says 89 percent of surveyed consumers expect to maintain or increase spending on pre-loved goods in 2025, with Gen Z at 59 percent and Millennials at 56 percent leading the increase. McKinsey’s work on social commerce described U.S. social-commerce purchases at $37 billion in 2021 and projected nearly $80 billion by 2025, with younger consumers particularly active in buying without leaving a platform. What this means for collectibles is straightforward: the marginal buyer is younger, more feed-native, more comfortable with creator-led trust, and more accustomed to shopping in environments where entertainment and transaction are fused. The classic search-era middle-class collector still exists, but he is no longer the sole engine of liquidity for the $50–$500 band.

For a mixed inventory of sports cards, ALS, true-crime pieces, and historical artifacts, this bifurcation is even harsher than it is for pure card inventory. Cards at least have population reports, public comps, and standardized categories. A signed letter from a second-tier historical name or a niche true-crime relic often has none of that. So the item falls into the worst possible liquidity lane: not cheap enough to be an impulse purchase, not famous enough to be a trophy, and not standardized enough to ride algorithmic ranking or industrial trust rails. That is where the middle-class collector used to matter most. That is also where market support has clearly weakened.

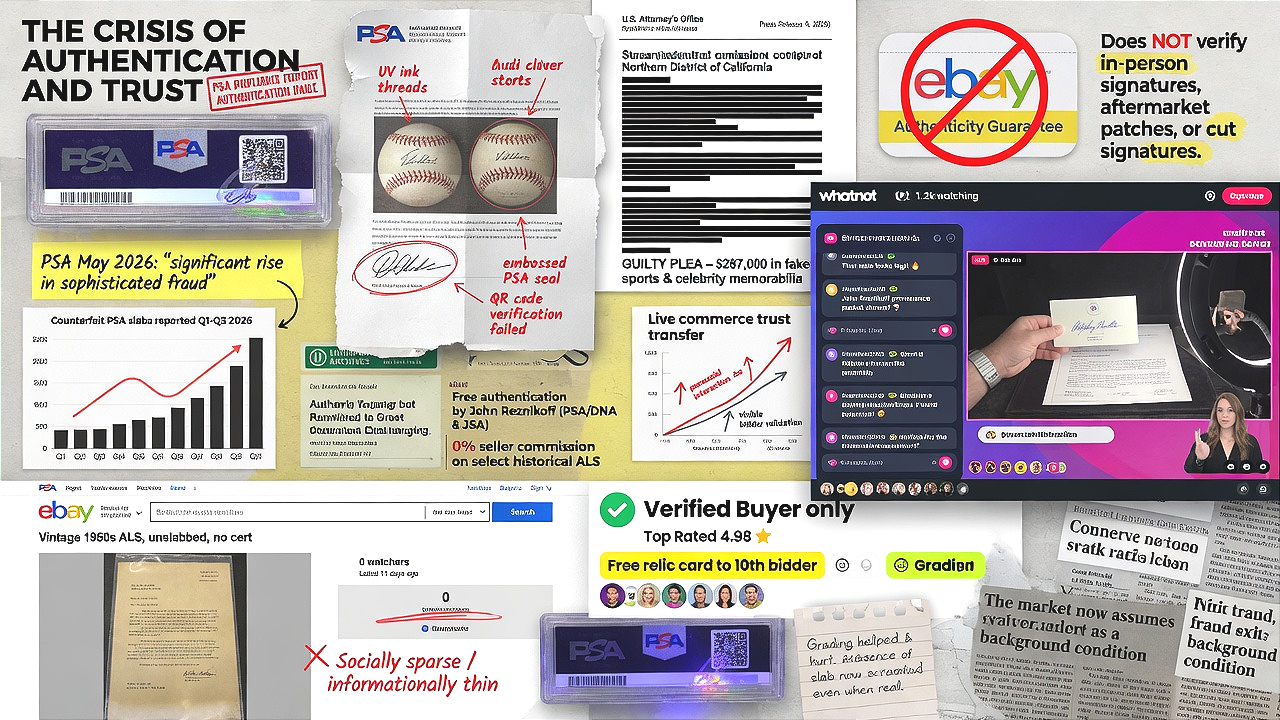

The Crisis of Authentication and Trust

The trust problem is no longer theoretical. PSA’s May 2026 infrastructure announcement says the surge in collecting has been accompanied by a “significant rise in sophisticated fraud and counterfeiting.” PSA also maintains a buyer’s guide specifically warning collectors about counterfeit PSA-certified items and how to inspect labels and holders. Federal enforcement activity confirms that the category remains live: in 2025 the U.S. Attorney’s Office in California announced a guilty plea involving hundreds of thousands of dollars in fake sports and celebrity memorabilia, and in late 2025 the Northern District of California announced a guilty plea in a fraudulent sports-memorabilia case as well. The lesson is not that fraud is new. It is that the market now assumes fraud as a background condition, especially in signatures and memorabilia.

That makes trust wrappers central. PSA advertises itself as the largest autograph authentication service and says it has certified over 35 million collectibles; its photographic-authentication paperwork emphasizes anti-counterfeit security features in the letter itself. Specialist houses make the same point from a different angle. University Archives markets “competitive seller’s fees,” notes that on some material it charges no seller commission, and explicitly emphasizes free authentication through John Reznikoff, a long-time expert for PSA/DNA and JSA. In other words, institutional trust is now part of the product being sold. For ALS and historical artifacts, the paper, provenance packet, and expert name are often as marketable as the object.

The problem is that platform trust rails are unevenly distributed. eBay’s trading-card Authenticity Guarantee is real and useful, but its own rules state that for cards with in-person signatures or aftermarket patches and relics, the inspection does not verify the autograph or the aftermarket addition itself. That is fine for standard cards. It is a material limitation for signed cards, cut signatures, unusual relic formats, and memorabilia-adjacent material where the signature or attached piece is the whole point. In those categories, a seller cannot assume that presence of the checkmark solves the buyer’s trust problem.

Grading culture has helped and hurt at the same time. It has helped because population reports, condition census data, and standard holders reduce some information asymmetry. Classic research on online auctions found that seller reputation is one market mechanism that can alleviate information asymmetry, and related work on online trust-building showed that third-party trust mechanisms matter in auction environments. But grading culture also trains buyers to distrust whatever is not standardized. Once buyers are accustomed to slabs, verified returns, vault custody, and approved graders, ungraded niche material can feel not romantic but risky. The absence of a slab or a recognized authenticator becomes an adverse signal, even when the object is perfectly legitimate.

Live commerce has exploited that gap. McKinsey describes live commerce as blending entertainment with instant purchase and audience participation, and it argues that the format can meaningfully compress the path from awareness to conversion. Academic work is even more direct: Frontiers studies on live-streaming commerce show that interactivity, entertainment, and visualization catalyze trust transfer; parasocial interaction and social presence increase impulsive purchase tendencies; streamer interaction increases cognitive trust; and visible comments or other buyers’ behaviors operate as social cues that build confidence. Whatnot operationalizes exactly these dynamics. It allows fixed-price and auction selling during streams, supports giveaways, measures seller quality and fulfillment rigorously, and lets hosts require Verified Buyers to cut down troll bids. That package makes a static auction listing feel thin by comparison.

Traditional listings therefore feel outdated for two reasons at once. First, they are informationally sparse relative to what modern buyers now expect: live inspection, narrative context, reactions from other bidders, and visible seller competence in real time. Second, they are socially sparse: no chat, no community, no momentum, no proof that others are watching or validating the item. That does not mean static auctions are obsolete. It means they now need additional scaffolding—authentication, provenance, specialist-house branding, or pre-sale audience warming—to feel safe enough for contemporary buyers. Pure “post and wait” is no longer a trust strategy.

Strategic Pivot

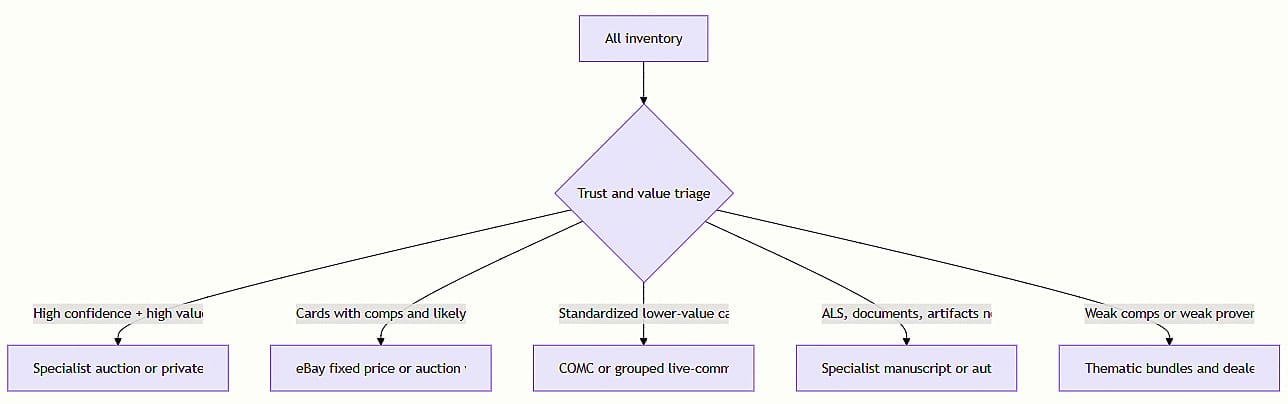

The practical pivot is to stop selling “an inventory” and start selling four different products: institutional-quality trophies, story-rich curated drops, outsourced standardized throughput, and bundled tail lots. The seller’s real asset is not just the objects. It is subject-matter knowledge across sports cards, documents, and niche memorabilia. In a discovery market, expertise has to be surfaced as programming. The right operating model is therefore not marketplace monoculture. It is channel specialization. That conclusion is a synthesis from platform ranking rules, fee structures, social-commerce behavior, and trust research.

This triage logic follows the way public platform thresholds and specialist channels are actually structured: eBay card authentication starts at $250, the vault begins at higher price points, Whatnot’s economics improve for high-value sales but its algorithm prefers active channels, COMC is strongest where standardization offsets its fee and cash-out structure, and specialist houses explicitly market authentication, price guidance, or direct purchase for manuscript-grade material.

Recommended channel mix

| Channel | Public cost structure | Expected velocity | Best use | Recommended action |

|---|---|---|---|---|

| eBay fixed price / offers / selective auction | Trading-card categories: 13.25% up to $7,500 plus per-order fee; optional ad spend if promoted | Medium | Cards with comps; authenticated memorabilia with broad search demand | Use for items that can benefit from eBay search and, where eligible, Authenticity Guarantee |

| Whatnot live | Sports Singles / Toys & Hobbies: 8% commission up to $1,500, 0% above that portion in current promo, plus 2.9% + $0.30 processing | High once audience exists; low without one | Bundles, lower-mid cards, performative selling, fast-cycle inventory | Do not build from zero alone; partner with an established streamer or run limited pilot shows first |

| COMC | 5% fixed-price fee; 5% auction fee; submission and storage fees; 10% cash-out fee | Medium to high for standardized singles | Operational outsourcing of the card tail | Use only for standardized cards where labor savings outweigh the cash-out drag |

| Specialist sports auction house | Often negotiated; stronger audience for elite material | Medium | Trophy cards, headline memorabilia | Reserve for top-end items only; do not feed it middle bulk |

| Specialist manuscript / autograph house | Often negotiated; some offer free authentication and even direct purchase | Medium | ALS, historical artifacts, niche signed material | Send a curated packet of strongest documents first and ask for both consignment and outright-buy indications |

| LiveAuctioneers through a partner house | House-dependent; platform markets bidder reach, anti-fraud, payments | Medium | Antiques, historical oddities, cross-category catalog material | Use through the right house if catalog fit is clear; not as a primary DIY card channel |

| Owned audience | Processor-level costs only, but marketing effort is high | Low initially, rising over time | Narrative pre-selling, collector retention, drop support | Build as support infrastructure for drops, not as the only near-term liquidity channel |

The cost and mechanics in this table come from the public fee and platform pages; the velocity estimates are directional inferences based on discovery mechanics, channel specialization, and operational frictions rather than guaranteed outcomes.

Authentication and grading strategy

| Inventory type | Recommended trust action | Rule of thumb | Why |

|---|---|---|---|

| Sports cards with clear comps and plausible sale price above $250 | Use eBay’s card-authentication rail; grade selectively | Grade only if expected net uplift clearly exceeds grading cost, delay, and selling friction | The $250 threshold unlocks a market trust wrapper that lower-price cards do not get |

| Sports cards below roughly $150–$200 | Usually do not grade individually | Sell raw via bundles, lots, or outsourced single-card channels | Grading costs now consume too much of gross proceeds on typical middle-tail items |

| Autographed cards with in-person signatures | Third-party autograph review if value justifies it | Treat as autograph problems, not generic card problems | eBay states its card Authenticity Guarantee does not verify in-person autographs themselves |

| ALS, signed documents, historical ephemera | Expert authentication, provenance packet, specialist cataloging | Prioritize named figures and strong stories first | For documents, the expert narrative and provenance are often inseparable from the value |

| Niche memorabilia or true-crime artifacts | Provenance-first, house review, policy screening | Avoid mass-platform listing until provenance is organized | These are the items most exposed to trust failure and lowest algorithmic legibility |

This is the crucial discipline point: do not grade because the hobby loves grading, and do not authenticate because buyers “might want it.” Grade or authenticate only when the trust premium is likely to be monetized by the channel you plan to use. PSA’s cost and turnaround disclosures, eBay’s $250 authentication threshold, and the autograph limitations on card authentication all make that triage necessary.

Tactical operating plan

The first move should be segmentation, not listing. Build a working manifest with six fields that matter commercially: item type, current authentication status, reasonable comp band, likely best channel, narrative strength, and operational friction. Then rank every item into four buckets: top 10 percent, next 20 percent, middle 40 percent, and tail 30 percent by expected net proceeds—not gross theoretical value. If an object needs six emails, uncertain comps, and a trust explanation to sell for $125, it belongs in a different bucket from a liquid $125 card single. Treat labor as real. That is what the current market does.

For sports cards, the best non-fire-sale path is a barbell. Send only the standardized tail into a throughput channel, either COMC or tightly scripted Whatnot/eBay-live lots, and reserve serious individual treatment for pieces likely to clear the trust and economic thresholds of the modern market. That means using eBay for cards whose likely sale price can exploit its search demand and trust rails, and using specialist auctions only for the handful of cards or memorabilia pieces strong enough to be catalog highlights. Do not consign the middle just because it is easier. Average items disappear in prestigious catalogs too.

For ALS and historical material, the correct play is to shift from item-centric selling to thematic curation. A one-off signed letter from a non-marquee name may stall. A small, tightly argued group lot around a theme—Civil War correspondence, underappreciated presidential aides, baseball-adjacent documents, crime history, or “letters that reveal process rather than signature”—can sell because the buyer is purchasing a thesis, not just paper. Specialist houses are better positioned for this because they bring authenticator credibility, catalog framing, and a standing bidder base that already shops one-of-a-kind material. University Archives explicitly offers both consignment and outright purchase discussions, which is useful because it lets the seller create a floor price without broadcasting distress. RR Auction’s immediate/private-sale pathway serves a similar purpose for quality pieces.

For live commerce, the key is not to become a full-time streamer. The key is to borrow audience and format. Because Whatnot’s discovery system rewards historical popularity and strong seller metrics, a cold-start account is structurally disadvantaged. The practical solution is collaboration: place 50 to 100 liquid, demonstrable items into one or two pilot sessions with an established host who already has category fit. Use those events for bundles, claim-style lots, and “story sets,” not for the most provenance-sensitive ALS pieces. The objective is fast cash conversion, price discovery, and market feedback—not prestige. Requiring Verified Buyers helps reduce non-paying or unserious bidding behavior.

For marketing, stop writing listings as inventory records and start writing them as distribution assets. TikTok and Instagram documentation is unambiguous that engagement, watch time, similarity, and user response drive distribution. That means every serious item or drop needs a short-form narrative asset: one vertical video, one provenance carousel or document zoom sequence, one clean hero photo, and one specific hook. “Rare signed letter” is not a hook. “A signed 19th-century letter revealing how the rumor spread after the event” is a hook. Discovery systems do not read value the way old collectors do. They read attention. The seller has to translate scholarship into media.

For pricing, use a three-lane framework. Use specialist-auction estimates and reserves only for top-end material with institutional trust support. Use fixed-price-with-best-offer on eBay for items with comp depth and search demand. Use clear no-reserve or low-opening-price event lots only where velocity matters more than individual item price precision. The middle path is not “price everything high and wait.” It is “price to create negotiation without signaling desperation.” For historical material with weak comps, obtain at least two outside indications—one from a specialist house and one from a dealer or private-buyer network—before setting public pricing.

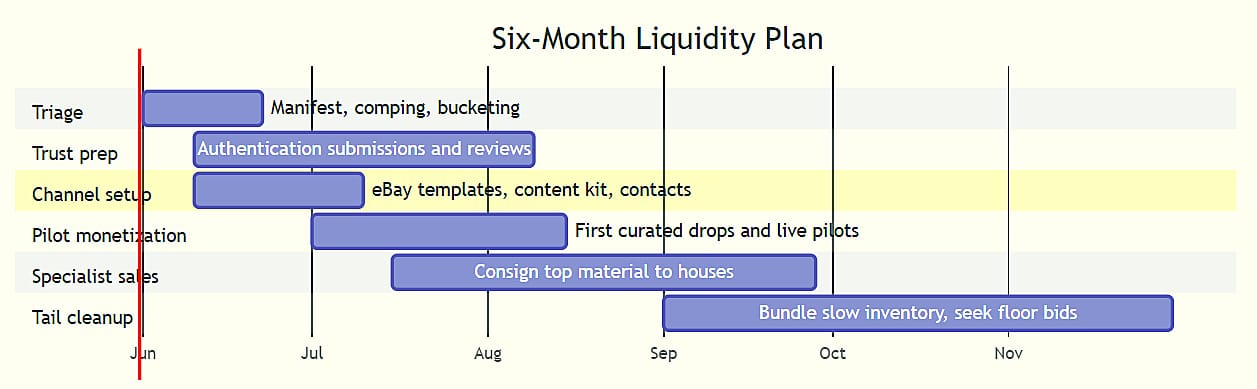

Phased implementation

| Phase | Priority work | Output | Success test |

|---|---|---|---|

| First month | Manifest, triage, comp review, house outreach | Inventory ranked by net-liquidity bucket | 100% of items assigned to a channel lane |

| Second month | Authentication decisions, listing templates, content packaging | Trust-ready top cohort and first drop calendar | At least one live pilot and one eBay drop launched |

| Third month | Specialist consignments and second wave of drops | Top material in the right houses; middle inventory in market | Sell-through improving without blanket discounting |

| Months four through six | Bundle and purge tail, negotiate dealer floors, recycle lessons | Reduced listing count, higher average realized value per labor hour | Inventory count down materially while margin is preserved |

This phased cadence is a synthesis, but it is grounded in public realities: grading turnarounds, live-commerce ramp requirements, specialist-house workflows, and the need to front-load trust work before asking algorithms or bidders to do the rest.

The blunt recommendation is this: do not try to liquidate 500 items through one interface. Put the best 25 to 40 items into institutional trust channels, the next 75 to 125 into curated eBay and collaborative live-commerce drops, the standardized card tail into outsourced throughput, and the weakest 20 to 30 percent into thematic bundles with a clear floor-bid strategy. That is how you avoid a visible fire sale while still forcing the collection to convert into cash. The market no longer rewards patience by default. It rewards packaging, proof, and programming.

Open Questions and Limitations

This report is grounded in current public platform documentation, industry data, and academic research, but it does not include the actual inventory manifest, recent sell-through history, average asking prices, present authentication status by item, or any negotiated commission schedules that a seller might obtain from houses or consignment partners. Because of that, the channel mix and timeline are high-confidence strategy, not a line-item forecast.

The weakest evidentiary area is exact realized-price behavior for the specific kind of mixed historical and true-crime inventory described here. Public data are far denser for trading cards than for niche documents and artifacts. For those categories, the report leans more heavily on platform mechanics, trust theory, and specialist-house positioning than on a large public comp dataset.

References

Ba, Sulin, and Paul A. Pavlou. “Building Trust in Online Auction Markets through an Economic Incentive Mechanism.” Decision Support Systems, 2003.

Card Ladder. “1986 Fleer Michael Jordan Base #57 PSA 10.” 2026.

Card Ladder. “1952 Topps Mickey Mantle Base #311 PSA 1.” 2026.

Card Ladder. “1952 Topps Mickey Mantle Base #311 PSA 9.” 2026.

Card Ladder. “Indexes.” 2026.

COMC. “COMC Consignment Rates.” 2026.

eBay. “Authenticity Guarantee for Trading Cards.” 2026.

eBay. “eBay Standard Envelope.” 2026.

eBay. “Optimize Listings for Best Match.” 2026.

eBay. “Promoted Listings Overview.” eBay Developers Program. 2026.

eBay. “Selling Fees.” 2026.

eBay. “Selling with Authenticity Guarantee.” 2026.

eBay. “The 2025 Recommerce Report.” 2025.

eBay. “The Listing Quality Report.” 2026.

eBay Inc. “eBay Launches Its Vault for Trading Cards.” 2022.

Frontiers in Communication. “Examining the Impact of Parasocial Interaction and Social Presence on Impulsive Purchase in Live Streaming Commerce Context.” 2025.

Frontiers in Communication. “Socio-Technical Systems and Trust Transfer in Live Streaming Commerce.” 2024.

Frontiers in Communication. “Streamer Interaction and Consumer Impulsive Buying in Live-Stream E-Commerce.” 2025.

Frontiers in Psychology. “Integrating Social Presence with Social Learning to Promote Purchase Intention in Live Streaming Commerce.” 2022.

Jin, Ginger Zhe, and Andrew Kato. “Price, Quality and Reputation: Evidence from an Online Field Experiment.” 2005.

McKinsey & Company. “It’s Showtime! How Live Commerce Is Transforming the Shopping Experience.” 2021.

McKinsey & Company. “Ready for Prime Time? The State of Live Commerce.” 2023.

McKinsey & Company. “Social Commerce: The Future of How Consumers Interact with Brands.” 2022.

Meta Transparency Center. “Instagram Reels Chaining AI System.” 2025.

PSA. “An Update on Pricing and Services at PSA.” 2026.

PSA. “Authentication.” 2026.

PSA. “PSA Announces $200 Million Infrastructure Investment to Support Global Demand.” 2026.

PSA. “PSA Security: A Buyer’s Guide.” 2026.

RR Auction. “Immediate and Private Sales.” 2026.

RR Auction. “Why Consign to RR Auction.” 2026.

TikTok Newsroom. “How TikTok Recommends Videos for You.” 2024.

TikTok Newsroom. “5 Tips for TikTok Creators.” 2024.

University Archives. “Sell or Consign Your Collection.” 2026.

University Archives. “Selling Details.” 2026.

U.S. Customs and Border Protection. “$1.4M in Fake Sports Merchandise Seized by Cincinnati CBP.” 2025.

U.S. Department of Justice, Central District of California. “Former West Covina Resident Pleads Guilty to Selling Fake Memorabilia to Professional Athletes and Other Victims.” 2025.

U.S. Department of Justice, Northern District of California. “Concord Man Who Sold Fraudulent Sports Memorabilia Pleads Guilty to Wire Fraud.” 2025.

Whatnot. “Premier Shop Program.” 2026.

Whatnot. “Start Selling on Whatnot.” 2026.

Whatnot. “Understand How Discoverability Works on Whatnot.” 2026.

Whatnot. “Whatnot Seller Fees.” 2026.

Whatnot. “Require Verified Buyers during Your Show.” 2026.